{kind=link}

Ensure your investment is secure with our comprehensive real estate due diligence checklist before closing. Learn essential steps to protect your interests.

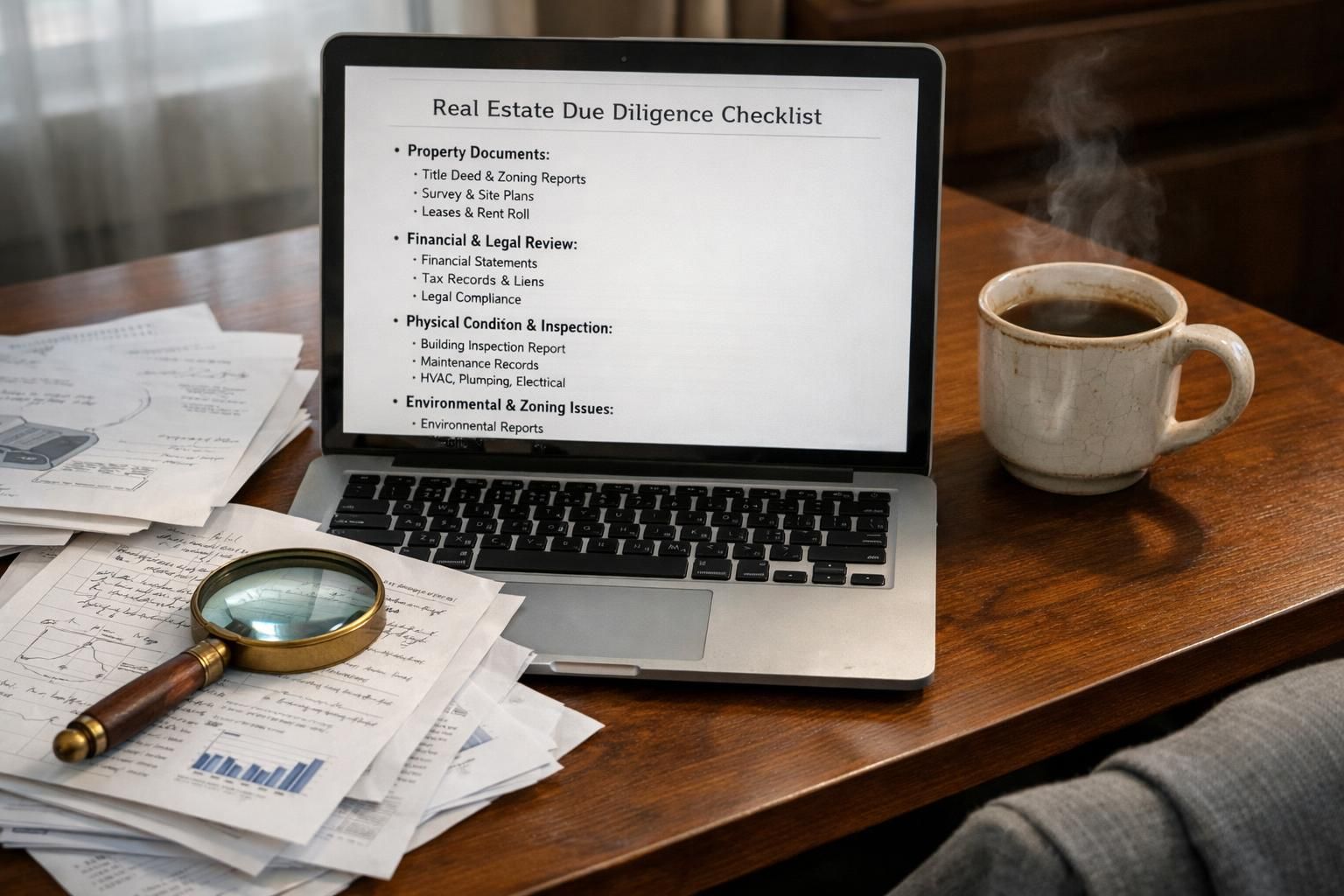

Table of Contents

- Review Legal Documentation

- Evaluate the Property's Physical Condition

- Financial and Contractual Review

- Compliance and Zoning Checks

- Risk and Safety Assessments

- Understanding Wholesale and Wholetail in Real Estate

- Identifying and Marketing to Motivated Sellers

- Final Steps Before Closing

- Conclusion

- FAQs

Real Estate Due Diligence Checklist Before Closing

Many real estate investors rush to closing, only to face costly surprises later. Missing key checks in your real estate due diligence checklist before closing can threaten your investment and peace of mind.

This article gives you a clear road map, showing every step you need for smart property decisions. You will learn how home inspection, title search, land survey, environmental assessments, zoning rules, and HOA regulations protect your interests.

As a partner at Robertson & Williams in Oklahoma City with years spent guiding clients through complex transactions, I have seen what thorough due diligence must include. You will find proven tips that work in the field.

Turn these insights into actions as you get ready for success—read on now.

Key Takeaways

- Always review legal documents, title reports, HOA rules, and survey maps before closing. This step helps catch issues like liens, lawsuits, or missing seller authorization that can delay deals or cause financial losses.

- Get a certified home inspection and land survey to find hidden problems. Inspectors check for foundation damage or deferred maintenance. Land surveys confirm acreage and property boundaries—mistakes here could lower value by thousands of dollars.

- Confirm all contracts, insurance policies, tenant leases, and utility bills are accurate. Failing to spot gaps can lead to unexpected costs such as high HOA fees (sometimes $200–$300 per month in 2024) or unpaid taxes that affect your ROI.

- Check zoning codes and local development plans using GIS maps and county websites. New city projects might change how you use the property or reduce future profits if regulations shift unexpectedly.

- Complete environmental assessments for old buildings (pre-1980) to avoid costly cleanups tied to hazards like asbestos or soil contamination. Lenders often require these reviews before approving loans; ignoring them risks legal action later (sources: FEMA.gov flood data, www.ncrec.gov state guidance).

Review Legal Documentation

Check all legal documents to confirm clear ownership and accuracy in the title report. Spot issues like pending lawsuits or errors in seller authorization to avoid future risks during your real estate investment.

Seller Authorization

Seller authorization proves the seller’s legal right to transfer real estate. Always require Articles of Incorporation, Articles of Organization, and any amendments if the seller is a business entity.

Do not skip Bylaws or Operating Agreements since these documents show how decisions are made within the company. Review all amendments as well because many investors have seen deals fall apart over missing paperwork.

Request a complete schedule of owners and confirm that everyone with authority has approved the sale. Insist on Certificates of Good Standing from state agencies to confirm compliance with state tax laws and registrations.

Reliable sellers will present annual filings with the Secretary of State, copies of fictitious or assumed name registrations, and proof that they own those names.

Experience shows disputes can occur if beneficial ownership is unclear in mergers and acquisitions or commercial real estate transactions. Take time to cross-check every document provided during due diligence; this step prevents delays at closing and reduces risk for you as a buyer or investor.

These requirements help protect your investment by ensuring clean title transfer free from undisclosed claims or fraud risks often found during background checks or title search reviews.

Title Report

A title report verifies the ownership history of a property. Title search professionals review deeds, examine past sales records, and look for any legal claims against the parcel. You need to check for liens or unpaid taxes that could disrupt your purchase.

Unpaid property taxes from a previous owner can lead to foreclosure notices or lawsuits and delay closing.

Always request copies of current property deeds and existing title policies as part of your due diligence checklist. Confirming legal descriptions is crucial so you avoid boundary disputes after buying.

Review maps and obtain recent surveys to ensure no encroachments affect access or use rights.

Look closely at restrictive covenants tied to homeowners association (HOA) rules, as these can limit what you do with the land or building. Document all easements, rights of way, and possible utility access issues in your review process.

Clear title allows smooth transfer of ownership without future challenges over market value or lawful possession. In my experience working with investors since 2015, ignoring small details in a title report once resulted in unexpected HOA fees surfacing months after closing—a mistake no one should repeat on their next investment deal.

Pending or Threatened Legal Actions

Check for any schedule of existing or potential litigation involving the property, seller, or related parties. Review details about each case, including involved parties and the nature of their claims.

Confirm whether there are known contingent liabilities, administrative proceedings, or government investigations attached to the asset. List labor disputes affecting either ownership or operations.

Make sure you have documentation on agreements with collection agencies regarding lawsuits against the seller. Identify injunctions and court orders that restrict what the owner can do with the real estate.

Carefully examine contracts made between family members or interested parties during your due diligence process; these could signal hidden risks. Include all broker agreements and pending commissions in your review so unexpected costs do not arise before closing.

Back to topEvaluate the Property's Physical Condition

Inspect the property's structure to uncover deferred maintenance and assess true market value. Use a property condition assessment alongside environmental site assessments to reveal issues that may impact your investments or future operations.

Home Inspection

A home inspection helps you avoid costly surprises and protects your real estate investment. A licensed home inspector provides a visual evaluation of the property’s main mechanical and physical systems.

- Request a certified home inspector to assess the home’s roof, foundation, HVAC, electrical, plumbing, and structure.

- Get a property condition assessment to spot deferred maintenance, water damage, or faulty wiring early.

- The inspector examines basement areas to detect moisture issues or signs of foundational problems that could impact property value.

- Review the inspection report with your broker to understand issues such as roof durability or possible drainage concerns.

- After you analyze the results, choose to move forward as-is, renegotiate with the seller for repairs or credits, or terminate the purchase agreement if risks outweigh benefits.

- Submit written repair requests that specify required work and request proof such as receipts once repairs are complete.

- Failure to resolve major issues may affect safety, livability, long-term return on investment, and future appraisals or insurance costs.

- Thorough inspections help reduce risks related to title reports and improve confidence in closing decisions.

Land Survey

Land surveys protect your investment during real estate due diligence. You get a clear report showing exact property boundaries, total acreage, building locations, and nearby encroachments.

Lenders often require you to purchase the survey before closing; it safeguards financing by confirming property details on the title report.

You must check set-back lines and zoning restrictions through a land survey before signing a purchase agreement. This prevents costly violations or unwanted surprises after closing.

Imagine planning for three acres but discovering only 2.5 acres once the survey is complete—that miscalculation can drastically alter property valuation and potential use.

A land survey exposes easements, rights of way, or public access points that affect usage options and long-term value of your asset. Clear knowledge of utility easements, roadways, or shared driveways ensures compliance with all building codes and local regulations.

In my experience as an investor working with multiple lenders since 2018, resolving disputes over boundary lines early avoids legal headaches later on—especially in areas where underground storage tanks trigger phase I environmental site assessments as part of environmental regulation compliance steps.

Environmental Assessments

Review Phase I Environmental Site Assessments (ESAs) to spot soil contamination, asbestos, or lead paint. Properties built before 1980 can contain hazardous materials like asbestos or lead-based coatings that put buyers and insurers at risk.

Urban sites often face issues with PCBs and other toxic substances.

Examine inspection documents for disclosure of physical hazards and check compliance records from local agencies for any past violations. Secure full reports on hazardous waste disposal procedures and infectious or hazardous waste agreements if the property was used for industrial purposes.

Lenders require thorough environmental assessments to protect against unexpected cleanup costs and safety risks before closing a real estate transaction.

Back to topFinancial and Contractual Review

Review financial statements and contracts to uncover hidden costs, check insurance coverage, and verify property management agreements—these steps help you protect your bottom line and make smarter investment decisions.

Explore the next section to maximize your advantage.

Home Appraisal

A certified appraiser assesses the true market value of the property based on its current condition and sale prices of comparable homes. This unbiased valuation considers local market trends, recent upgrades, unique features, and deferred maintenance.

If the appraisal comes in at $450,000 but your purchase agreement is for $500,000, you must cover the $50,000 difference or renegotiate with the seller.

Lenders require a home appraisal before they approve mortgage loans or real estate financing. Accurate valuations protect you from overpaying for a property that does not meet projected returns or cash flow goals.

Appraised values also impact key factors like property taxes and hazard insurance requirements. Use this information to guide financial modeling and economic analysis while evaluating potential return on investment for your target market.

Existing Leases and Tenant Agreements

Collect all relevant documents for leased properties. Secure copies of leases, subleases, assignments, and any related instruments before you close. This documentation helps you understand tenant rights, capital expenditures responsibilities, and ongoing financial obligations tied to the property.

Request up-to-date rent rolls if the asset generates rental income. These records allow you to analyze profit and loss statements and forecast cash flow with accuracy.

Interview tenants whenever possible. Conversations often reveal hidden issues like deferred maintenance or neighborhood safety concerns that might not appear in a home inspection report.

Ask direct questions about the landlord’s reliability with repairs or disputes over pricing and utilities. Always review contracts for compliance with anti-money laundering laws as well as for obligations such as insurance premiums, flood insurance requirements, or pending environmental assessments.

Evaluate how existing tenant agreements will affect your management transition plan. Subleases may add layers of legal complexity; assignments could trigger future negotiations under current local development plans or zoning rules.

Clear understanding here gives you leverage during purchase agreement discussions and helps ensure a smoother transfer of ownership once due diligence is complete.

Contracts, Insurance, and Utilities

Strong contract and insurance reviews protect your real estate investment. Check all utilities and service agreements to avoid surprises at closing.

- Review every construction, improvement, repair, and maintenance contract connected to the property. These contracts outline the obligations for deferred maintenance or future repairs.

- Examine service or maintenance agreements, such as those for elevators, HVAC systems, or security monitoring devices. Look for patent or copyright licensing terms that could impact property use.

- Inspect purchase agreements for clauses on environmental assessments, home warranty coverage, and adjustable-rate mortgage options.

- Obtain a schedule of current insurance policies showing each insurer’s name, policy expiration dates, coverage amounts, deductibles, and premiums. Compare the list with other properties in similar locations.

- Request copies of homeowners insurance policies or self-insurance agreements linked to the asset. Check policy exclusions related to climate risk or flooding events.

- Analyze any pending or threatened insurance claims involving this address. Claims can reveal issues like soil contamination or previous flooding.

- Confirm documentation of current claims filed with insurers along with details of existing reserves held against these claims. Accurate reporting helps you assess financial risks before closing.

- Evaluate utility bills for electricity, water, gas, internet access points, and cell reception quality across the site. Bills highlight energy efficiency issues that can impact expenses over time.

- Assess historic records for recurring infrastructure problems like frequent power outages or high water usage. Maintenance logs may uncover chronic concerns such as a leaky roof that could result in future legal action from tenants.

- Measure operational costs by reviewing HOA fees and rules governing common area utilities managed by homeowners associations (hoas). Prompt review can prevent budget overruns due to unexpected HOA assessments.

First-hand experience shows thorough due diligence gives investors a clear edge during negotiations. You will quickly uncover hidden costs tied to contracts and utilities while protecting your reputation in real estate transactions.

Back to topCompliance and Zoning Checks

Check all rules and zoning codes before you buy. Use the county website and GIS maps to make sure your real estate deal meets local laws and land use plans.

Zoning Rules and Restrictions

Zoning rules drive how you can use and change a property. Local governments set these restrictions to guide growth and protect neighborhoods. Single-family zoning, for example, blocks the conversion of homes into multi-unit rentals.

Failing to follow these regulations can result in costly fixes or legal action.

Always read the title report and perform a full title search before closing. Review all restrictive covenants tied to the land or recorded with the county. Confirm that building set-backs meet city codes so you avoid future disputes.

Inspect for encroachments on neighboring lots since violations may limit your rights or cause access issues.

Experience shows zoning approvals, variances, and use permits are critical documents in due diligence. Missing even one approval can halt renovations or new construction projects entirely.

Zoning also affects long-term value if local plans change allowed uses; commercial investments face real risk when city councils adopt new policies without warning investors first.

This step protects your investment and gives peace of mind at closing time.

Homeowners Association (HOA) Rules

HOA rules can significantly impact a real estate investment. You must review all HOA documents before closing. These will outline restrictions on property use, exterior changes, and leasing policies.

Many associations set limits on short-term rentals or home modifications that could affect your business model or exit strategy.

HOA fees make up a major part of the monthly budget for single-family homes. The average ranges from $200 to $300 per month in 2024 but some properties charge more. Overlooking these costs will distort your financial assessment and reduce future profit margins.

Examine annual dues, special assessments, late fees, and reserve fund health to avoid surprises down the road.

Disputes with homeowners associations often lead to legal action or compliance headaches later. Failure to follow bylaws may result in fines or litigation which delays sales and raises expenses.

Understand how association rules influence rental plans, resale timing, and overall value so you can plan confidently and maximize return on investment during due diligence checks.

Local Development Plans

Local development plans can change the economic environment around your property. City or county agencies often post area forecasts and future projects, like parks, highways, commercial spaces, or industrial zones.

New NCDOT infrastructure projects may bring increased traffic, noise, and even new competition. Use sources like https://ncdot.gov/projects to track upcoming changes.

Review these plans carefully before closing any real estate deal. Future developments might boost neighborhood growth or trigger a decline in property values. Proactive engagement with local planning departments lets you predict trends that could impact value or use of your investment.

Smart due diligence here helps you adjust your purchase agreement and forecast returns based on solid data rather than guesswork.

Back to topRisk and Safety Assessments

You must conduct thorough risk and safety assessments to protect your investment. Use tools like flood zone maps, ESG data, and cell coverage checkers to spot issues before they affect the deal.

Flood History and Natural Disaster Risks

Flood risk can transform a property's value and appeal. Properties near rivers, lakes, or in low-lying areas often sit within federally designated flood zones. FEMA.gov gives clear flood maps so you can identify these risks fast during your real estate due diligence process.

If the property falls inside a flood zone and a loan is needed, lenders will likely require flood insurance as part of your purchase agreement.

Review all available records for past floods, earthquakes, tornadoes, or wildfires that have touched the site. Even if federal maps do not place the address inside a high-risk area, extreme weather events may still pose threats to both property insurance costs and future resale values.

Investors benefit from considering proactive disaster prevention steps like drainage improvements or fire-resistant landscaping.

Flood history connects directly to ongoing expenses such as higher premiums for home insurance policies and mandatory coverage requirements under federal guidelines. This information influences investment decisions by signaling potential financial risks beyond standard title searches or environmental assessments.

Strong knowledge of local hazard trends will build trust with buyers and strengthen your position when explaining market viability to partners or investors.

Noise and Nuisance Checks

Multiple visits to the site at different times clarify real estate due diligence. Check noise during rush hour, local events, nightlife, or school activities. Airports, highways, commercial businesses, and livestock farms can generate serious noise pollution that impacts property desirability.

Analyze both daytime and nighttime patterns to assess how noise levels shift.

Review complaints from former tenants or owners and include those details in your title report. Evaluate if nuisance issues such as persistent loud music or traffic require soundproofing or mitigation measures before closing the purchase agreement.

High levels of unwanted sound may reduce home value and lower tenant satisfaction over time.

Noise considerations play a critical role for residential investment properties. Excessive disturbances sometimes create ongoing legal risks tracked through environmental assessments or flagged in HOA reports.

Factor these findings into your overall financial analysis to ensure strong tenant retention and future property appreciation.

Internet and Cell Reception

Test the internet and cell reception onsite as part of your real estate due diligence. Strong connectivity stands as a modern must-have for buyers and tenants. Use online tools such as broadband coverage maps from providers like AT&T or Verizon to double-check signal strength at the property location.

Walk through every room with your mobile device to check data speeds and call clarity.

Poor service can decrease property desirability, lower resale value, or cause problems with emergency communications. Tenants expect reliable high-speed access in both single-family homes and multifamily units.

If you identify dead zones or weak signals during home inspection, plan for extra costs such as installing boosters or negotiating infrastructure upgrades with internet carriers. Solid wireless performance gives your investment a strong edge in any market, making it stand out in listings and targeted advertising campaigns.

Back to topUnderstanding Wholesale and Wholetail in Real Estate

Wholesale and wholetail real estate strategies create valuable investment opportunities, but both carry specific risks. Wholesale involves securing a property under contract below market value and then assigning that purchase agreement to another buyer for a profit.

Wholetail deals use a hybrid approach, where you buy the property at a discount, make minimal repairs or none at all, and resell quickly on the open market. Due diligence helps uncover market gaps so you can act fast with confidence when evaluating wholesale or wholetail investments.

You must review all legal documentation like the title report and confirm seller authorization before moving forward with these methods. Pay careful attention to existing leases, insurance coverage, pending lawsuits, compliance requirements such as zoning rules or homeowners association (HOA) restrictions, and physical inspections including home inspection reports or environmental assessments for issues such as soil contamination.

The North Carolina Real Estate Commission offers extra guidance at www.ncrec.gov if you need help adapting your strategy by state. This level of preparation arms you with clear knowledge to mitigate risk while pursuing economic growth through smart real estate transactions.

Back to topIdentifying and Marketing to Motivated Sellers

Sellers with encumbrances, liens, or ongoing litigation often show clear signs of motivation. Disclosure forms may reveal mineral, oil, or gas rights have been severed; always request more details if marked “Yes.” Watch for properties in a flood zone since this affects insurance costs and the buyer’s risk profile.

As an investor performing real estate due diligence, review each title report to spot any unexpected claims.

You should focus on targeted marketing strategies that address specific seller pain points. Properties governed by restrictive covenants or homeowners association (HOA) rules need unique messaging.

Use direct mail campaigns and social media adverts to reach owners facing deferred maintenance or high HOA fees. Automated email systems allow you to follow up quickly once you identify motivated sellers through public records or online credit reporting databases.

Aim your message at their needs to inspire them to start negotiations sooner rather than later.

Back to topFinal Steps Before Closing

Give each disclosure a second look and match details against your title report or purchase agreement. Make sure you have all legal documents, credit scores, and insurance details ready for a smooth final transaction.

Cross-verify Disclosures

Cross-check all property disclosures against the results of your home inspection, land survey, and title report. This step helps you spot any gaps or conflicts in what the seller reports versus what professionals find during real estate due diligence.

Review disclosures on issues like structural defects, flood zones, mineral rights, and environmental hazards such as soil contamination. Compare these details with public records to ensure truthfulness.

Ask for supporting documents if a seller marks “Yes” to any disclosure item that could affect value or use; pay attention if they choose “no representation.” Examine HOA restrictions and covenants for alignment with your goals as an investor.

Make sure all agreements about utilities, insurance coverage, existing leases, and ownership transfers are accurate before closing. Confirm that every discrepancy is resolved since even small errors can cause legal disputes later.

Confirm all Contingencies are Met

Check that all contract contingencies are resolved before closing. Review the purchase agreement to verify inspection, appraisal, and financing conditions have been satisfied within your set deadline.

Confirm all repairs agreed upon in writing are complete. Ensure receipts for work and documentation of methods used are on file.

Review reports from your home inspection, surveyor, phase II environmental assessments, and any structural engineering as needed. Make certain title insurance, zoning compliance, homeowners association (HOA) rules, and required insurance documents align with requirements listed in the agreement.

Examine tenant agreements or rent rolls if rental units exist on site. My experience shows that overlooking a single contingency can stall deals or trigger legal disputes; thorough verification keeps transactions on track and shields you from costly mistakes.

Ensure Smooth Transfer of Ownership

Obtain legal descriptions, deeds, and title policies for all real property before closing. Secure the assignment of any contracts, existing leases, or subleases to protect your rights as the new owner.

Confirm that all insurance coverage transfers correctly; keep documentation ready for easy reference.

Register the property transfer with your state’s Secretary of State or local authorities based on regulations in your area. Settle any outstanding liens, mortgages, and claims to avoid future disputes over ownership or payment.

Collect all keys, access codes, maintenance agreements, and possession documents at closing to guarantee full control from day one.

Transfer utility accounts into your name so there are no interruptions after you take possession. Make sure escrow agents finalize payments exactly as stated in the purchase agreement and closing statement.

Following these steps secures a smooth transition and protects both financial investment and legal standing in every real estate transaction.

Back to topConclusion

You unlock real value and protect your investment with a strong real estate due diligence checklist. By reviewing title reports, home inspections, HOA rules, and environmental assessments, you lower your risks before closing.

Focus on contract details, financial checks, and compliance to avoid costly surprises later. A careful approach helps you secure the property with confidence while staying prepared for future opportunities in this field.

Always seek professional advice tailored to your specific needs for best results.

Back to topFAQs

1. What is real estate due diligence before closing?

Real estate due diligence means checking important facts about a property before you buy it. This process includes reviewing the title report, confirming property boundaries, and making sure the purchase agreement matches your needs.

2. Why should I order a home inspection as part of my checklist?

A home inspection helps reveal deferred maintenance or hidden problems in the house. It gives you details on repairs needed so you can plan or negotiate with confidence.

3. How do title search and title report protect buyers?

A title search and title report confirm that no one else has legal claims to your new property. They help prevent future disputes over ownership and verify that all records are clear for transfer.

4. Should I look into environmental assessments during real estate due diligence?

Yes; environmental assessments check for soil contamination or other hazards on site. These steps support strong environmental, social, and governance (ESG) practices while protecting your investment from costly surprises later.

5. Why review homeowners association (HOA) rules and fees before closing?

Understanding HOA fees, rules, and restrictions will affect your monthly costs and daily living experience in the community. Reviewing these documents ensures there are no unexpected obligations after logging in as a resident or using shared amenities like pools or clubhouses.

Back to top